08/08/23

Do you possess personal life insurance and have a limited company? You could save a significant amount through tax relief by transferring the payment of your personal life insurance cover to your company. In this article, our knowledgeable financial advisors in the Private Client Team explain what Relevant Life Protection is and how business owners can benefit from it.

What is Relevant Life Protection?

- Relevant Life is an insurance policy that a business can take out to provide life insurance for an individual employee, including employed directors.

- The aim is to provide a lump sum benefit on the death of a single employee.

- The amount of Relevant Life cover that can be applied can be up to 35 times your combined income from salary and dividends, depending on age.

- The policy is designed to meet the requirements of a single life policy under S393B (4) (b) of the Income Tax (Earnings and Pensions) Act 2003.

- Relevant Life Protection provides great benefits, whereby the insurance premiums are paid by your limited company before taxes are applied, therefore attracting tax relief!

You could potentially make great savings via tax relief, by switching Your Personal Life Insurance Payment to the Company.

The benefits of Relevant Life Protection:

- Relevant life cover is tax deductible and not classed as a P11D benefit-in-kind by HMRC. Therefore, premiums paid via the company will have no further income tax and national insurance contributions applied.

- Premiums can be applied as a legitimate business expense and tax deductible against corporation tax.

- The payout received from relevant life policies are free from income tax and inheritance tax.

Relevant life policies are set up in a discretionary trust at the start of the plan, with the employees’ family or dependents as beneficiaries. This helps to ensure money paid out from a relevant life plan will not form part of the estate of the person covered, helping to minimise inheritance tax where applicable. Money paid out from the policy will not incur lengthy legal processes, such as needing to attain Grant of Probate. The trustee becomes the legal owner of the policy; therefore, payment is made directly to the trustees following a successful claim. The trust allows some flexibility regarding who will benefit from the policy.

The limitations of Relevant Life Policies:

- A Relevant Life policy is not an income protection or critical illness policy.

- The policy must end before the person covered reaches the age of 75.

- Once set up, the plan cannot be changed.

- If you cease contributions, then cover will lapse.

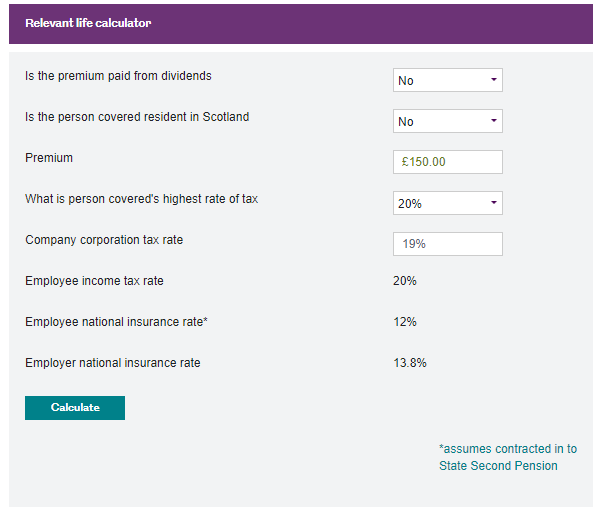

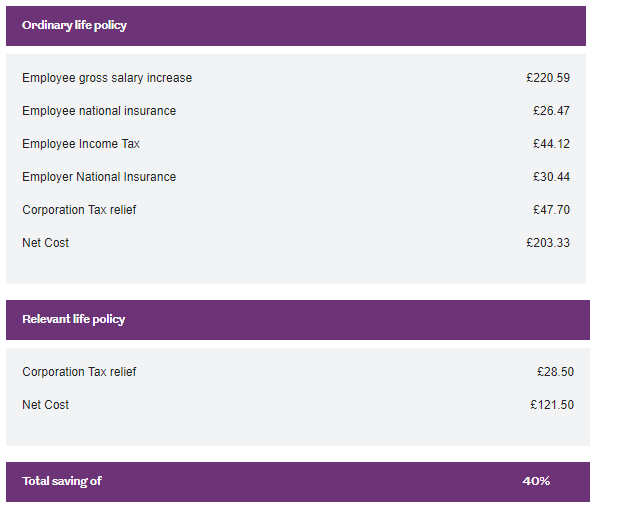

Meet Dave!

Dave holds a limited company but has taken out Personal Life cover for £500,000. His monthly premiums are £150. If Dave switched from personal cover to a Relevant Life policy, he would potentially be making a saving of 40%. The tables below are taken from Royal London and are for illustrative purposes only:

Take the first step towards maximising your tax savings today by speaking to one of our approachable financial advisors from our Private Client Team.